Venture History

Modern venture history begins with General Georges Doriot’s American Research and Development (ARD) Corporation. ARD invested in a wide range of novel technologies, from off-shore oil and radiation detection to, most importantly, minicomputers. As Tom Nicholas notes in his VC: An American History, ARD’s value grew at an attractive 15.8% compound annual growth rate. But, if you remove their investment in Digital Equipment Corporation (DEC), the developer of the first minicomputer, from the portfolio, ARD’s annual growth falls to 7.4%, failing to beat the S&P in the same period. DEC alone created as much value as the rest of the portfolio combined. This dynamic is not a fluke. Venture capital returns are driven by outlier investments. By investing in companies with capped downside and unlimited upside, venture funds maximize their returns by making high variance bets each with the potential to pay for the failures in the rest of the portfolio, potentially many times over.

In the wake of ARD’s success, other venture firms were established to search for DEC-like outliers. Venrock was founded in 1969, a few years after DEC’s IPO, and invested in Intel the same year. Kleiner Perkins was founded the year after Intel’s IPO and found early success investing in Genentech, the developer of the first synthetic insulin. From its earliest days, venture capital funded a wide array of technologies with the expectation that such new technologies could produce the kinds of extreme outcomes venture required.

The Software Moment

Over the last thirty years, venture has come to be more narrowly associated with software startups. The growth of the internet made it possible for every computer to communicate with every other. This connectivity meant software developers could write code once and immediately make it accessible to all of the businesses and consumers online. These internet software businesses had both a low cost to serve the marginal customer (all they had to do was cover server costs) and the ability to quickly iterate on their product based on customer feedback (instead of having to physically ship software on a floppy disk, internet businesses could quickly and cheaply update their code and immediately change the user experience).

The most important feature of the software internet business model was the potential for network effects. The internet made it possible for a single website to not just interface with the whole world but to help the whole world interact with each other, whether that meant commercially, socially, or to share information. Each user of a network benefits from the addition of each other user, which makes users want to join the largest networks, so the larger a network gets, the more users it attracts, creating a positive feedback loop. Amazon, Facebook, and Google were the breakout networks in their respective domains and have been able to maintain market dominance in the decades since their founding through the power of their network effects.

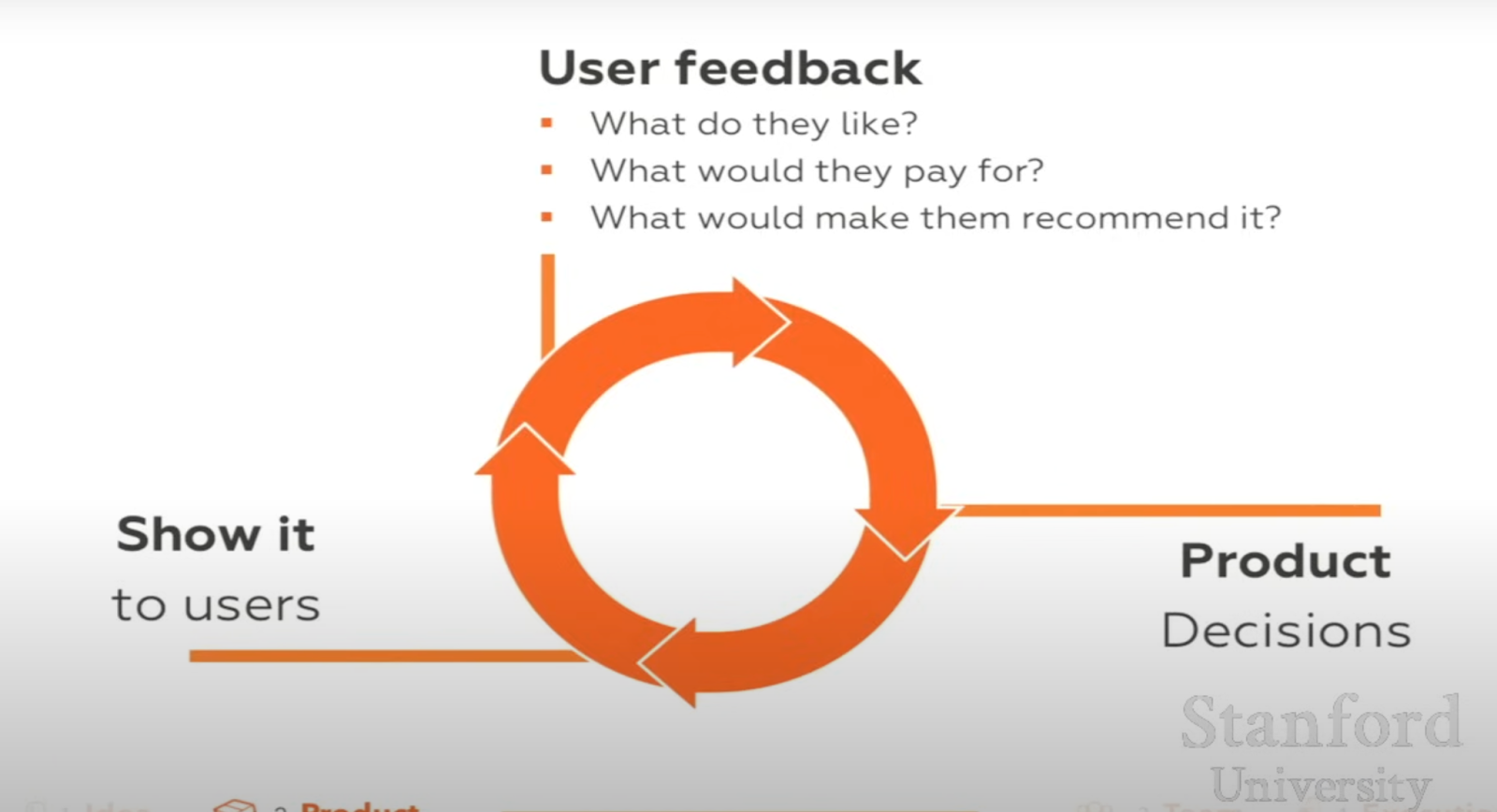

As these internet behemoths grew, venture capital focused more squarely on the internet software opportunity. Sam Altman nicely distilled the popular understanding of how great startups are built in his famous “How to Start a Startup” lecture. You hack something together quickly and cheaply, get user feedback, iterate on the product in light of that feedback, and let that process continue until you find product-market fit and grow enough to exit.

This strategy was unique to internet software companies whose minimum viable products could theoretically be built and deployed by as little as a single scrappy engineer. Venture became the way to finance the search for product-market fit for capital efficient, easy-to-iterate-on, quick-to-grow startups that could ideally defend themselves once they found product-market fit via network effects. We might call this dominant model the “lean startup” model.

Although the lean startup model has been successful over the last thirty years and has become near-synonymous with venture capital, it’s less well-suited to the mature era of the internet we’re in today and offers an overly restrictive conception of where venture capital can be profitably directed.

Lean software companies are best able to capture value when they can defend their business through the strength of their network effects since they don’t have strong technical differentiation. The thing about networks, however, is they largely only have to be built once. The late 90s/early 00s were very competitive in key areas like search, commerce, and social, but the dominant names in those spaces have been pretty stable since. While many justify investing in lean software through appeal to the amazing success of companies like Facebook, the reality is that the power of their network effect makes it harder to build new companies in that mold. No startup founded since Facebook has managed to become as valuable. Thirty years into the internet age, we have picked the low-hanging fruit of making the most valuable connections the internet enabled.

Instead of competing head-on with incumbent software networks, lean startups have carved out smaller niches made possible by new technology shifts, like mobile and AI. Uber seized the rise of mobile to connect a network of drivers and riders and was able to build a massive business doing so. However, Uber couldn’t simply use the lean startup playbook to conquer their niche. The mobile shift created intense competition to own the newly possible mobile-first networks, which forced Uber to spend huge sums of money to acquire users from lookalike competitors. Other mobile winners like Doordash followed a similar path. The capital efficiency leg of the lean model had to be set aside as companies iterated their way into the same niche and fought each other to reach network effect escape velocity first.

LLMs, the most recent major technology shift, are exacerbating the competition for users by making it easier to build software products. As the remaining networks left to connect get narrower and there are more players competing to own those narrow niches because of the ease of product development, outcomes in software networks will compress further. The LLM shift might turn out to most benefit incumbent foundation model owners. The foundation models could either reap the rewards of startups competing with each other to build thin wrappers on top of the models, or the foundation models might leverage their distribution advantages to vertically integrate and build new AI applications themselves.

Altman preached the lean startup gospel until he realized he did the exact opposite to build his most valuable venture: OpenAI. Instead of exploiting the ease of quickly and cheaply developing and deploying software products to iteratively find and address a customer’s unmet needs, OpenAI invested heavily upfront in solving profound technical problems and then was able to quickly commercialize their technically differentiated product.

None of this is to say the internet will not continue to be an exciting place or that interesting companies won’t be built there. On the contrary, I expect the future of the internet to be amazing and socially, culturally, and economically impactful. However, the one prescription of venture capital is to look for extreme outcomes wherever they might be. The dynamics that made lean startups built on the internet such a promising source of extreme outcomes over the last thirty years no longer hold. Venture’s historical success was investing in frontier-pushing technologies, and so as the lean startup opportunity compresses, the frontier might be the best place for investors to explore.

The Deep Tech Opportunity

“Deep tech” is the catch-all term for startups outside of the lean startup model. If lean startups search for a fit between a software product and an unmet need, deep tech startups figure out how to build something new that people need. Lean startups iterate with market feedback, deep tech companies iterate with technical feedback (“do people want this?” vs “does this work?”).1 There are very large markets that lean software companies haven’t and won’t transform: energy, manufacturing, defense, life sciences, telecom, semiconductors, etc. While lean software will continue to make life easier in these industries by improving workflows, the only path to radical improvements to their core products is through fundamental innovation in relevant fields like mechanical engineering, electrical engineering, chemistry, biology, etc. This is the territory of deep tech startups.

In theory, venture-backed deep tech startups could have emerged in these markets at any point in the last thirty years and competed with lean software startups for venture capital. However, these markets are under new transformative pressures today, making them especially ripe for disruption. The push to decarbonize, the growing threat from China, and the exploding demand for compute for AI are three mega-trends fundamentally reshaping the economy and pulling deep tech innovation forward. And in parallel to these social factors, the underlying technological primitives in many deep tech domains are quickly moving down cost curves, further accelerating deep tech progress.

Climate: Fossil fuels have helped drive global prosperity over the last 150 years. However, their combustion has released so much carbon dioxide into the atmosphere that we have changed its composition, trapping excessive amounts of heat. Responding to climate change will require mass electrification, making energy greener, replacing petrochemicals, decarbonizing hard to abate sectors, adapting to climate change’s inevitable effects, and drawing down emitted carbon from the atmosphere. These changes will necessitate new approaches to a wide range of massive industries like energy, steel, cement, transportation, agriculture, consumer goods, etc. The US and other governments are accelerating the transformation of those industries with R&D funding for new technology, carbon taxes, and subsidies for green approaches. Analysts expect trillions to be spent in the next decade building out climate infrastructure.

China: As the world opened itself up to globalization and free trade over the last thirty years, the US increasingly offshored its manufacturing capacity, much of it going to China. As geopolitical tensions have grown, there’s been an emerging bipartisan push to decouple from China and bolster American manufacturing capabilities, especially in strategically important industries. The new “Washington Consensus” seems to be pro-tariff and pro-industrial policy. The CHIPS act allocated hundreds of billions of dollars towards American semiconductor production, and the IRA ties its climate tech incentives to domestic manufacturing. These political pressures will demand technologists find new ways to produce strategically important goods in the US with its higher labor costs, tighter regulations, and available resources.

Compute: In 2019, Rich Sutton published “The Bitter Lesson”, arguing that progress in AI would come from techniques that leverage access to ever greater compute. The last five years are pretty good empirical validation of Sutton’s thesis. OpenAI launched the LLM era by scaling their GPT architecture from 117 million parameters in GPT-1 to 175 billion parameters in GPT-3. The promise of greater capabilities from scaling has pushed the entire industry to invest increasing orders of magnitude of capital in acquiring compute. Scaling models via large training runs and adding capacity for inference-time compute has led to the rapid buildout of new data centers, creating unprecedented demand for energy and enabling data center infrastructure.

As societal forces are driving demand for deep tech startups, secular trends in underlying technologies are making it easier to build compelling deep tech products. In energy, the costs of solar power and batteries have plummeted by approximately 90% over the last decade as production has exploded, allowing startups to design products premised on increasingly affordable energy generation and storage. Similarly, synthetic biology has experienced dramatic cost reductions in its fundamental operations of reading, editing, and writing genomes. The demand for compute as a societal force is driving demand for deep tech startups, and the stack those deep tech startups are developing has become a tool other deep tech startups can use. Hardware startups will leverage increasingly sophisticated simulation software to develop physical systems in silico, while frontier software companies in areas like computational biology and materials science are using the improving compute infrastructure to scale deep learning techniques for their respective domains. These trends are a few examples of the background conditions that have enabled deep tech startups to build products with tools incumbents lacked and around assumptions about the future the incumbents couldn’t model when they built the status quo.

Even if the mega-trends of the moment are putting pressure on legacy industries to innovate, one might still wonder if venture-backed startups are the right vector for that change. Maybe venture capital and deep tech are just incompatible, and public-private partnerships or incumbents’ R&D divisions are better equipped to tackle the opportunity.

There are existence proofs against the incompatibility of deep tech and venture capital. Nvidia and Tesla were both founded during the “deep tech winter” of the last thirty years and have gone on to become some of the most valuable companies in the world. In fact, there’s something about deep tech startups that is profoundly aligned with the venture model. Venture capitalists may have mistakenly developed a preference for companies that can persist on little capital as they iterate in search of product-market fit. Deep tech startups largely can’t do that. Early stage capital usually only lets them test one or two technical hypotheses. But, if a deep tech startup can crack whatever technical challenges they face, they should be uniquely positioned to upset a massive industry and rapidly gain market share. Such extreme binary outcomes reflect the core truth of venture: because downside is capped and upside is unlimited, all that matters is the size of the wins, not the recovery on the losses. The safety that venture investors have come to appreciate about investing in lean software might prove to be antithetical to the power law that undergirds the asset class.

Conclusion

Venture capital is the search for outlier companies. The decision of where to allocate the marginal venture dollar is grounded in belief about what kinds of companies might produce extreme returns. The era of lean startups producing tons of outlier returns by exploiting the ease of distributing and iterating on software to find product-market fit seems to be closing. Far from permanently redefining venture capital, the software moment might be remembered as an anomaly. As the lean startup opportunity compresses, however, the deep tech winter is thawing. Societal forces are creating unprecedented demand for fundamental innovation, while exponential improvement in key technological primitives has unlocked new branches of our tech tree. The future of venture might look a lot like a return to its past but with the benefit of the fruits of the software moment: investing in companies that create technically differentiated products with the help of cutting-edge software tools.

If you’re working on this future, I’d love to meet you.

- This distinction is not simply reducible to software vs hardware. While all lean startups are necessarily software companies, not all deep tech companies are hardware companies. There are technical frontiers in software that companies might raise venture capital to explore. AI, computational biology, and zero-knowledge proofs are examples of some such areas. The division between software and hardware is blurring too. Ostensibly hardware-focused companies are increasingly using software simulation for their system design, while software-focused companies like OpenAI are bottlenecked by physical limitations in compute and energy infrastructure. ↩︎

Leave a comment